Why Sustainability Without Energy Efficiency Fails in Data Centers

ENERGY DOMINANCE · WEEK 22 · PART II

The Costly Illusion of Green Energy Without Demand Reduction. And Why It Is Already Backfiring in 2026

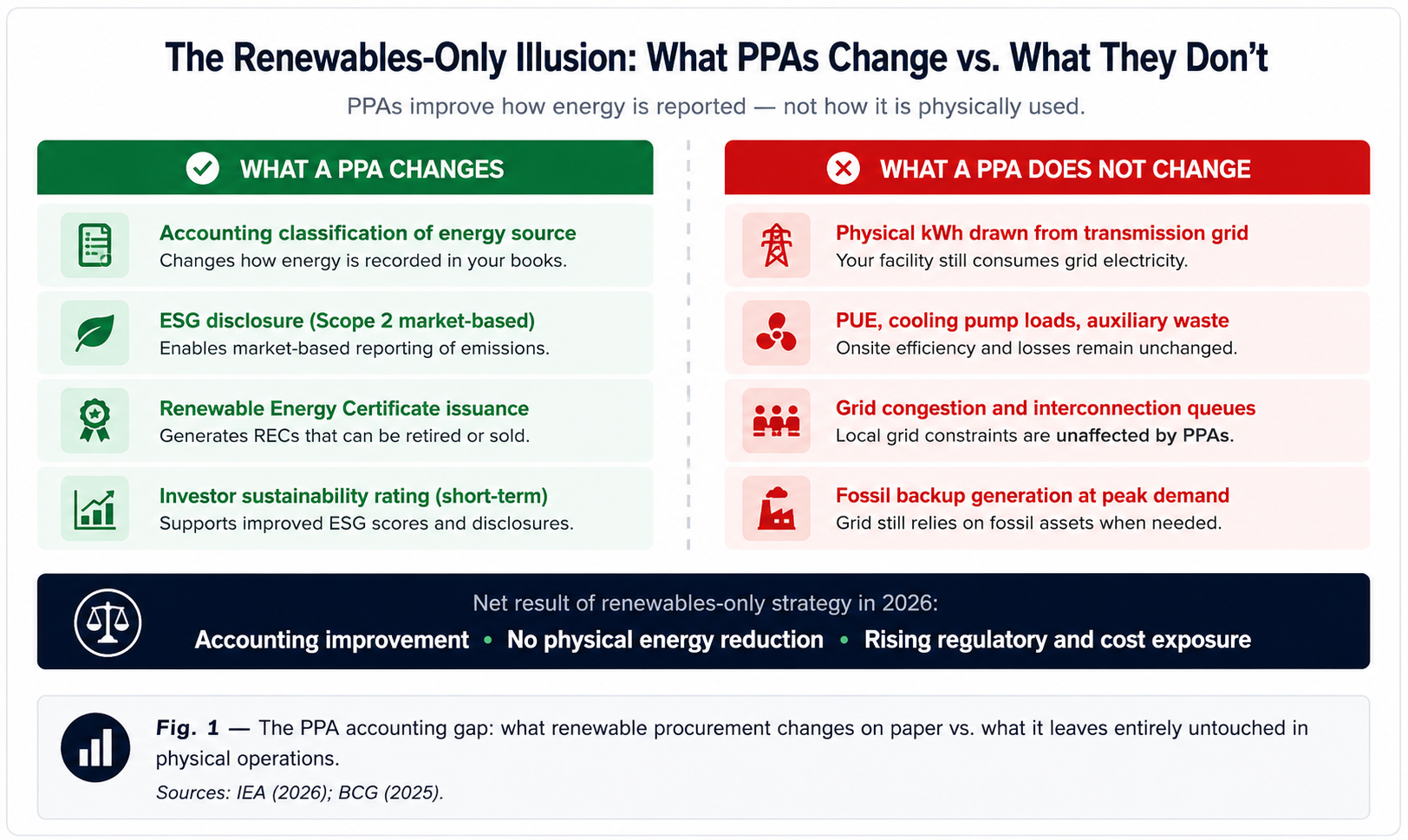

A renewable energy contract does not reduce a single kilowatt-hour of demand. It reattributes it, on paper, to a wind farm or solar array somewhere on the same grid that is simultaneously powering everything else. The data center still draws the same physical current, still runs the same fixed-speed cooling pumps, still maintains the same PUE of 1.5 or 1.6 or 1.8. The only thing that changed is the accounting entry. In 2026, the grid knows the difference. Regulators are beginning to know the difference. And the operators who built their sustainability strategy on procurement alone are discovering, at real capital cost, that an accounting trick is not an energy strategy.

② EXECUTIVE SUMMARY — IN 60 SECONDS

Global data center electricity consumption reached approximately 415 TWh in 2024 and accelerated by 17 % in 2025. Operators holding 100 % renewable PPAs are still driving grid congestion, fossil backup generation, and rising absolute emissions, because procurement does not equal efficiency.

The IEA's April 2026 report is unambiguous: without simultaneous demand reduction, renewable contracting inflates costs, extends grid interconnection queues by 18–36 months, and exposes operators to regulatory risk as absolute consumption rules replace source-only accounting.

Decision makers who make demand reduction, not renewable procurement, the primary sustainability lever will achieve lower TCO, faster permitting, verifiable ESG performance, and a structural competitive advantage in AI infrastructure deployment speed.

The Concrete Failure of Renewables-Only Strategies

The logic of a Power Purchase Agreement is compelling on a slide deck: procure renewable generation equivalent to 100 % of consumption, apply a Guarantee of Origin or Renewable Energy Certificate, declare carbon neutrality, and advance to the next ESG reporting cycle. The logic collapses on contact with the physical grid, and with the regulators who govern it.

A PPA does not modify a facility's draw on the transmission network. At moments of peak AI compute demand, precisely when grid stress is highest, data centers with high PUE values pull disproportionately large physical loads. The wind farm named in the PPA may be curtailed, geographically distant, or simply unavailable during that demand event. The grid response is fossil backup generation, demand-side congestion pricing, and interconnection queue extension. None of these appear in the Guarantee of Origin certificate. In 2025, facilities operating under 100 % renewable contracts but sustaining PUE values of 1.4–1.8 continued to drive new fossil-fuelled backup capacity additions at the grid level, with Scope 2 emissions remaining materially elevated and grid congestion increasing in high-density data center markets across Europe and North America.

The IEA's April 2026 report documents that absolute data center electricity demand surged 17 % in 2025, with renewable procurement outpacing efficiency improvement by a factor of approximately three, meaning the physical energy problem grew faster than any mitigation from green contracting. McKinsey's March 2026 AI infrastructure analysis confirms that operators in markets with PUE above 1.4 are experiencing grid interconnection delays averaging 18–36 months, regardless of renewable contract status. BCG's 2025 review identifies greenwashing regulatory exposure as an emerging material risk for operators whose sustainability disclosures rely predominantly on procurement-based metrics.

👉 Key Insight: Sustainability without energy efficiency is not neutral, it is actively counterproductive. It hides the underlying energy waste behind accounting attribution while the physical demand, the grid congestion, and the cost trajectory continue uninterrupted. In 2026, regulators are closing this gap. Operators who haven't are exposed.

Real-World Consequences Decision Makers Are Already Facing

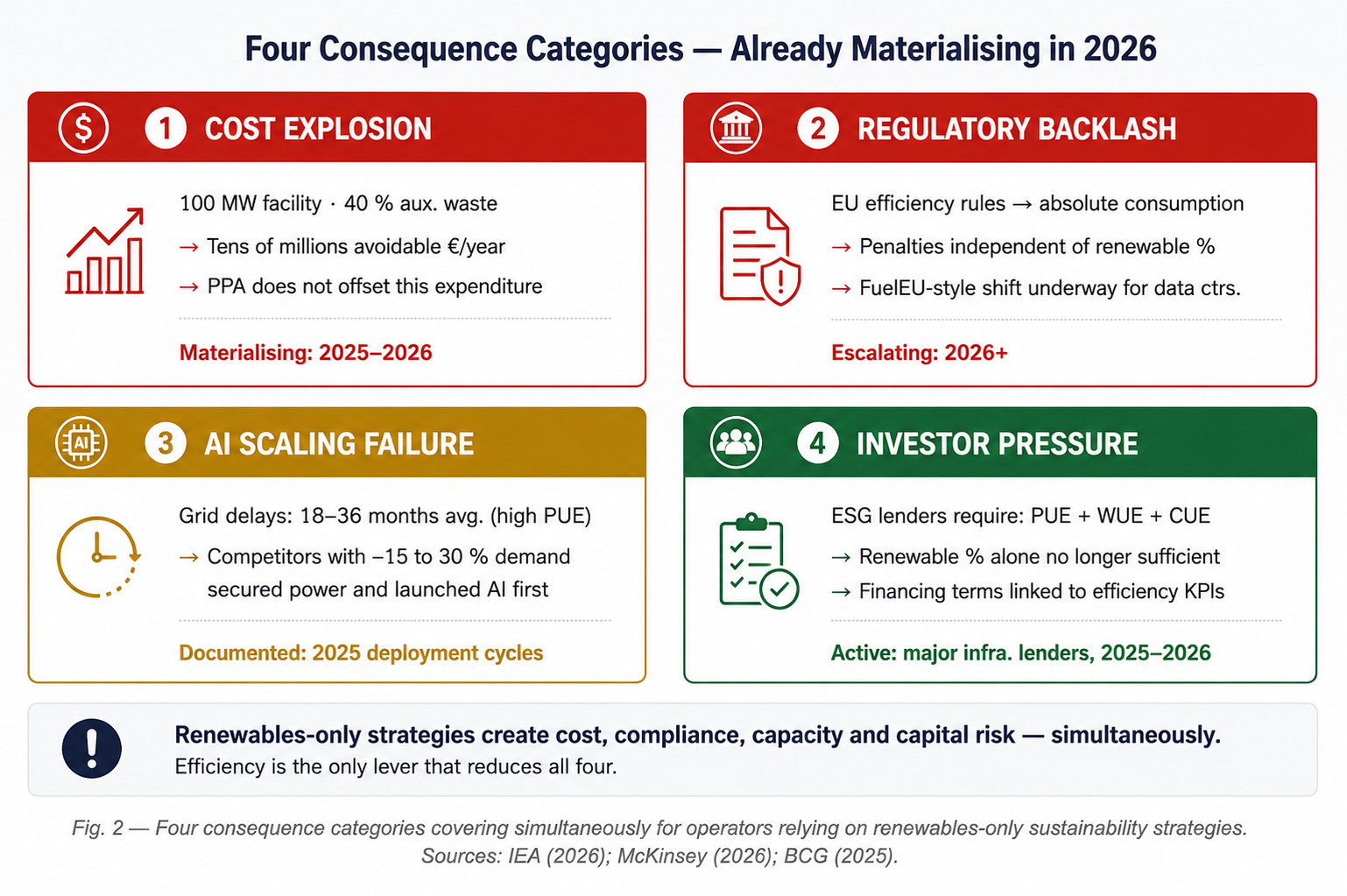

The costs of renewables-only sustainability strategy are no longer theoretical. They are appearing in capital budgets, interconnection timelines, regulatory filings, and financing term sheets, in 2025 and 2026, at material scale. Four consequence categories are converging simultaneously.

Cost explosion: a 100 MW AI data center sustaining 40 % auxiliary waste still pays for every one of those wasted kilowatt-hours regardless of the PPA. At European power pricing levels in 2025–2026, this represents tens of millions in avoidable annual expenditure that no renewable contract offsets. Regulatory backlash: EU energy efficiency directives and evolving sustainability disclosure obligations are shifting from source-accounting to absolute consumption rules, exactly as FuelEU Maritime shifted shipping from fuel-source accounting to carbon intensity per tonne-nautical mile. Facilities with high absolute consumption face penalty exposure independent of their renewable share. AI scaling failure: operators who deferred efficiency investment in favour of PPA procurement hit grid interconnection queues averaging 18–36 months, while competitors with 15–30 % lower demand profiles secured power agreements faster and launched AI services ahead of market. Investor pressure: major infrastructure investors and lenders in 2025–2026 are requiring verifiable operational efficiency metrics, PUE, Water Usage Effectiveness (WUE), and Carbon Usage Effectiveness (CUE), not merely renewable energy percentage claims, as conditions for favourable financing terms.

IEA's April 2026 analysis explicitly identifies the divergence between renewable procurement growth and efficiency improvement as a systemic risk to grid stability in high-density data center markets. McKinsey's 2026 infrastructure report quantifies the grid interconnection delay premium, 18–36 months, for facilities failing to demonstrate demand-side efficiency credentials. The Global Maritime Forum's 2026 operational review documents the direct regulatory parallel: shipping's transition from fuel-source to carbon-intensity accountability as the enforcement mechanism that finally forced demand-side action.

👉 Key Insight: These are not future risks, they are 2025 and 2026 capital events. Cost overruns, interconnection delays, regulatory exposure, and ESG financing constraints are hitting operators now. The window to correct the strategy is not indefinitely open.

Quantified Scenarios: What Actually Happens in 2026

Three strategies are available to data center operators pursuing sustainability in 2026. Their outcomes in cost, permitting speed, regulatory exposure, and genuine emissions reduction are not equivalent, and the divergence is now measurable.

The renewables-only path compounds existing problems: 17 % demand growth drives higher effective electricity costs despite nominal green procurement, grid bottlenecks extend interconnection timelines, and absolute consumption rules expose operators to greenwashing liability. The moderate efficiency path, 10–20 % demand reduction through VFD retrofits and basic demand-response optimisation, stabilises operations, accelerates permitting, and reduces TCO materially within 12–24 months. The efficiency-first sustainability path, 30–50 % reduction in auxiliary energy through liquid cooling integration, coordinated power distribution, and cross-functional governance, delivers genuine decarbonisation: lower absolute grid draw, lower Scope 2 on both market and location-based accounting, faster interconnection, and 20–40 % better financial return on every renewable contract in the portfolio, because each MWh of green energy is now covering a smaller, leaner physical load.

IEA 2026 modelling confirms that operators achieving PUE below 1.3 through integrated system efficiency face materially shorter grid interconnection queues than the industry average. McKinsey 2026 documents a 20–30 % permitting speed advantage for high-efficiency operators in competitive AI infrastructure markets. ABS and Wärtsilä retrofit documentation, applied to data center cooling and power distribution equivalents, supports the 30–50 % auxiliary energy reduction range for full system-level intervention, consistent with the maritime benchmark established in Part I of this series.

👉 Key Insight: The efficiency-first path does not merely improve sustainability credentials, it amplifies the financial return on every renewable energy contract in the portfolio. A leaner demand profile means each procured MWh of green energy covers more compute, delivers better Scope 2 performance per unit of AI output, and competes more effectively for limited grid capacity. Efficiency makes renewables work harder.

Make Efficiency the Foundation of Sustainability

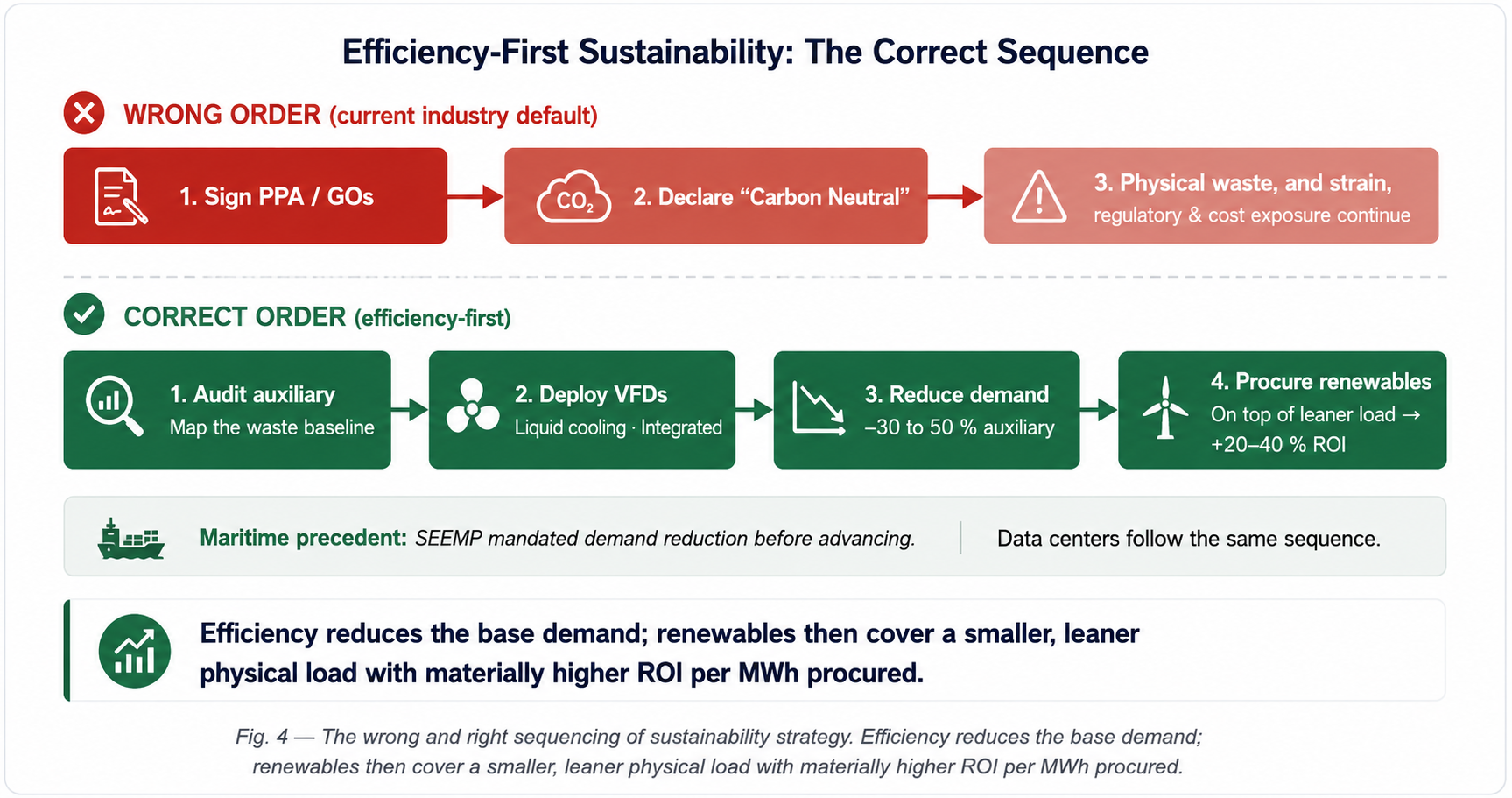

The corrective move is not to abandon renewable procurement, it is to sequence the strategy correctly. Efficiency first, then renewables on top of a reduced base. This is not a novel idea. It is the sequence that shipping regulators enforced through SEEMP and carbon intensity indexing, and that shipping operators eventually internalised as commercial strategy. The data center sector has the advantage of watching shipping make this transition first.

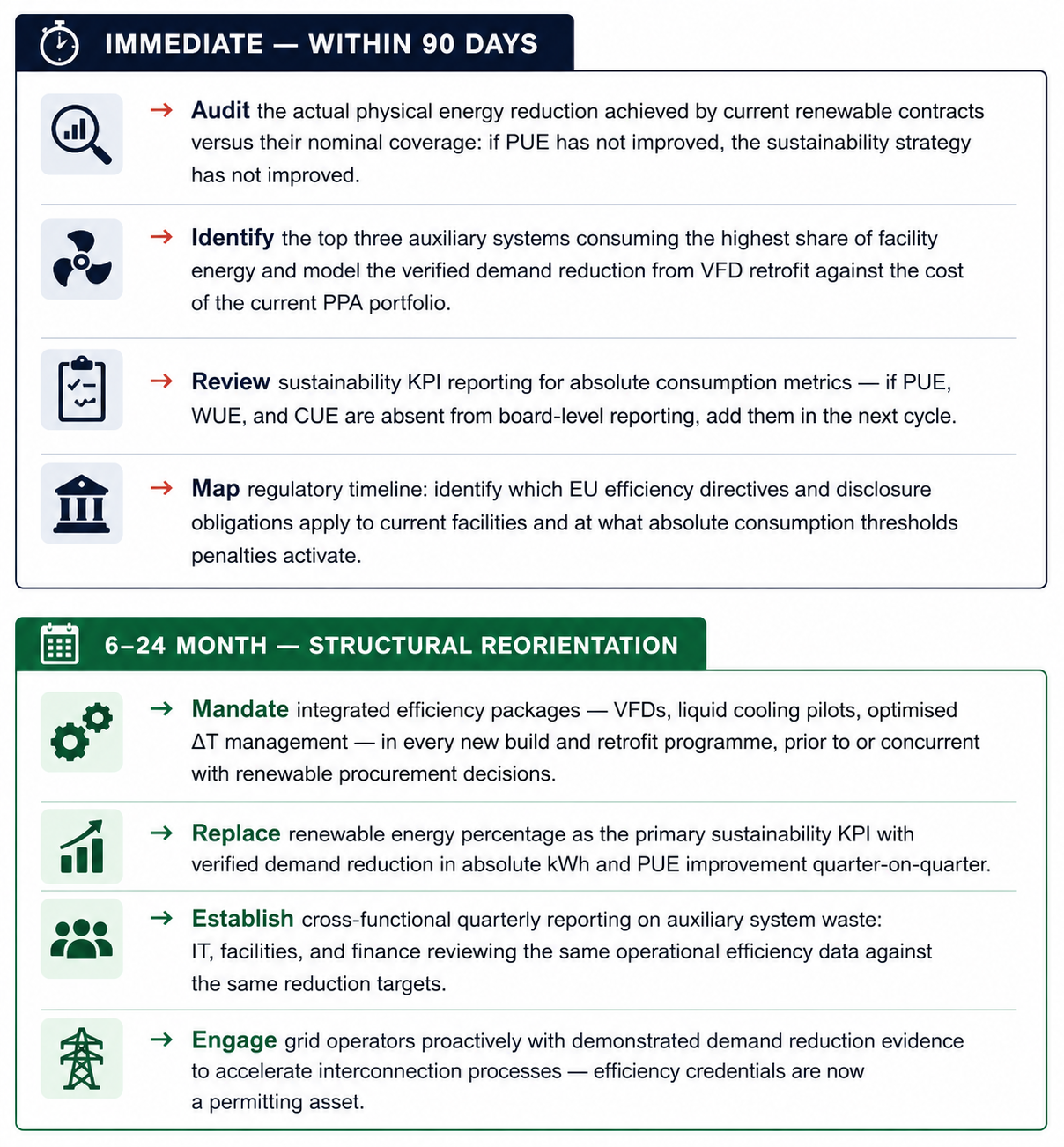

Four structural corrections reorient the sustainability strategy. First: retire renewable procurement as the primary sustainability KPI. Replace it with verified demand reduction, measured in absolute kWh, PUE improvement, and auxiliary load percentage. Second: mandate integrated efficiency packages in every new build and retrofit cycle. VFDs on cooling pumps, liquid cooling for high-density AI racks, optimised delta-T management in chilled water loops, these are the interventions that create the physical energy reduction that no PPA can replicate. Third: link sustainability KPIs directly to measurable energy demand reduction, not renewable percentage. This is the metric set that regulators are moving toward, that lenders are already requiring, and that genuine decarbonisation demands. Fourth: require cross-functional quarterly reporting on auxiliary system waste, IT, facilities, and finance in the same room, against the same numbers. This is the governance structure that made SEEMP effective in shipping and that makes efficiency gains durable rather than episodic.

McKinsey 2026 confirms that operators with integrated energy governance report verifiably lower absolute consumption and faster ESG disclosure audit cycles. IEA 2026 highlights demand reduction, not procurement substitution, as the primary lever for sustainable data center growth without grid destabilisation. The Global Maritime Forum's 2026 operational efficiency review documents SEEMP's enforcement mechanism, absolute carbon intensity, not fuel-source percentage, as the model that regulators in multiple jurisdictions are studying for direct adaptation to data center regulation.

👉 Key Insight: Efficiency does not compete with renewable procurement, it amplifies it. Every percentage point of demand reduction makes the renewable contract cheaper to honour, the ESG disclosure easier to defend, and the grid interconnection queue shorter. Sequence matters: efficiency first, renewables on top.

Actions for Decision Makers

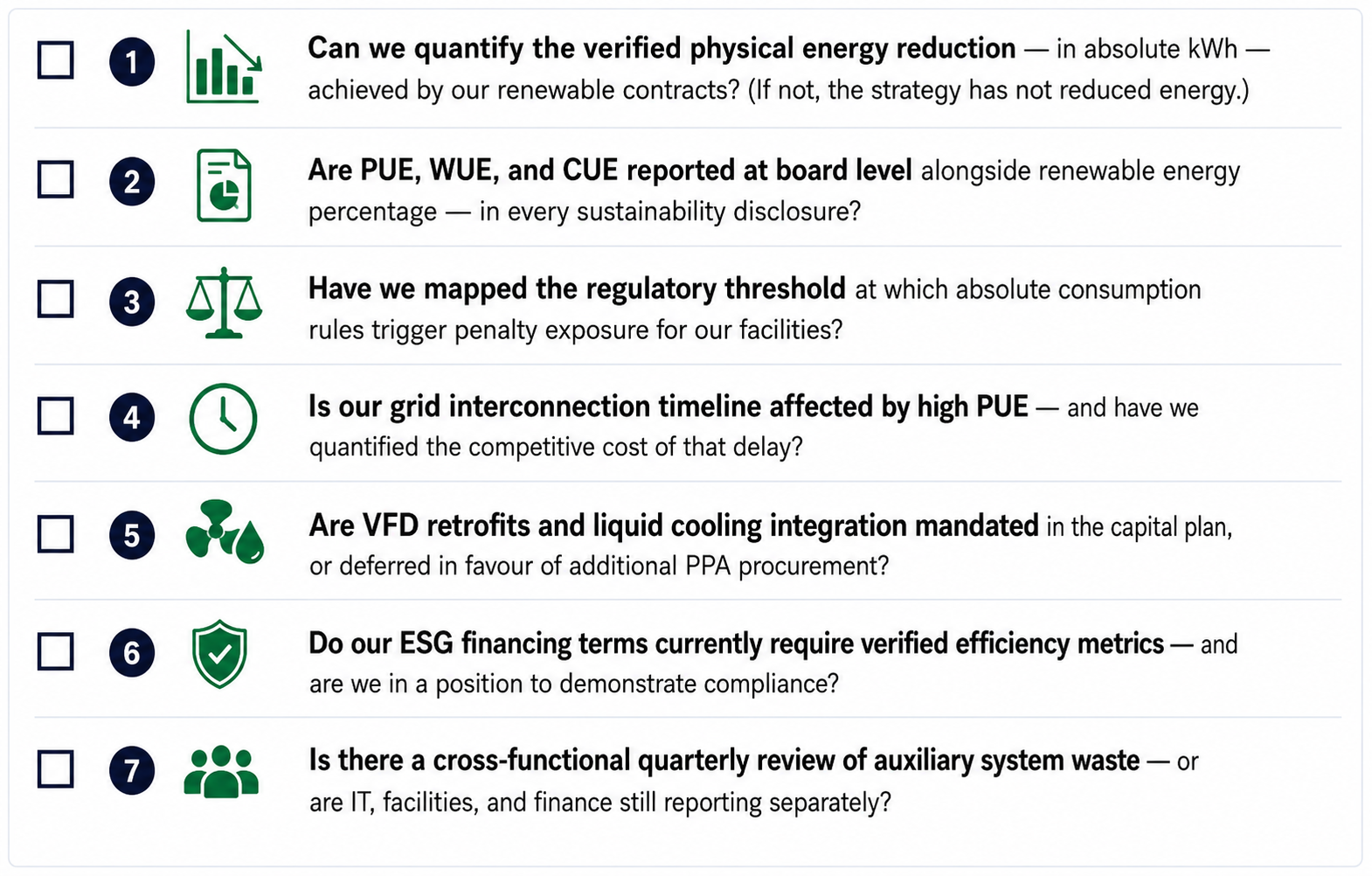

Leadership Checklist

A renewable energy certificate is not a substitute for a kilowatt-hour not consumed.

The operators who understood this first, who made demand reduction the foundation and renewables the amplifier, are now permitting faster, financing cheaper, disclosing with confidence, and deploying AI ahead of the queue. The operators still counting procurement percentages are discovering that the grid, the regulator, and the lender have moved on. Systems don't fail. Decisions do. The decision to treat efficiency as a prerequisite to sustainability is available in this capital cycle. Waiting for the regulatory mandate is the more expensive version of making the same choice.

WHAT'S YOUR NEXT MOVE?

Take the Next Step

Subscribe to the Weekly Punch for weekly strategic clarity, direct to your inbox.

References

International Energy Agency (2026). Key Questions on Energy and AI. IEA, Paris. April 2026.

International Energy Agency (2026). Data Centre Electricity Use Surged in 2025. IEA, Paris. April 2026.

International Energy Agency (2025). Data Centres and Data Transmission Networks — Electricity Consumption. IEA, Paris.

McKinsey & Company (2026). The $7 Trillion Race for AI Data Center Infrastructure. McKinsey Global Institute, March 2026.

BCG (2025). Breaking Barriers to Data Center Growth. Boston Consulting Group.

Global Maritime Forum (2026). Maritime Operational Efficiency Review. Global Maritime Forum, January 2026. Applied framework: regulatory transition from source-accounting to absolute consumption metrics, adapted to data center sustainability regulation.

ABS & Wärtsilä (2026). Vessel Auxiliary System Retrofit Performance Documentation. Applied framework: data center cooling and power distribution equivalents.

Note: This article reflects my personalviews based on industry experience and publicly available information. It does not constitute professional, legal, or investment advice and does not represent the views of my employer.