The Next Industrial Shift: AI, Energy, and Data Center Infrastructure

ENERGY DOMINANCE · WEEK 23 · PART II

Why energy mastery and data center infrastructure, not just AI algorithms, will separate the winners from the laggards in the coming decade.

DATA CENTERS | NEXT INDUSTRIAL SHIFT | JUNE 2026

Where Part I dismantled the false choice inside a single facility's budget, Part II steps back to the skyline. The story everyone is telling about AI is a story about chips and models. The story that will actually decide who leads the next decade is about something far less glamorous: where the power comes from, and how little of it is wasted. Electricity and the internet did not reward the companies with the cleverest machines, they rewarded the ones who mastered the infrastructure underneath. AI is no different. The next industrial revolution will not be won in the model layer. It will be won in the energy-and-infrastructure layer, and most boards are still treating that layer as plumbing.

This is Part II of Week 23: the macro view. Data centers are the new factories. Energy is the new raw material. And mastery of both is about to become the sharpest line between market leaders and the companies watching them pull away.

EXECUTIVE SUMMARY

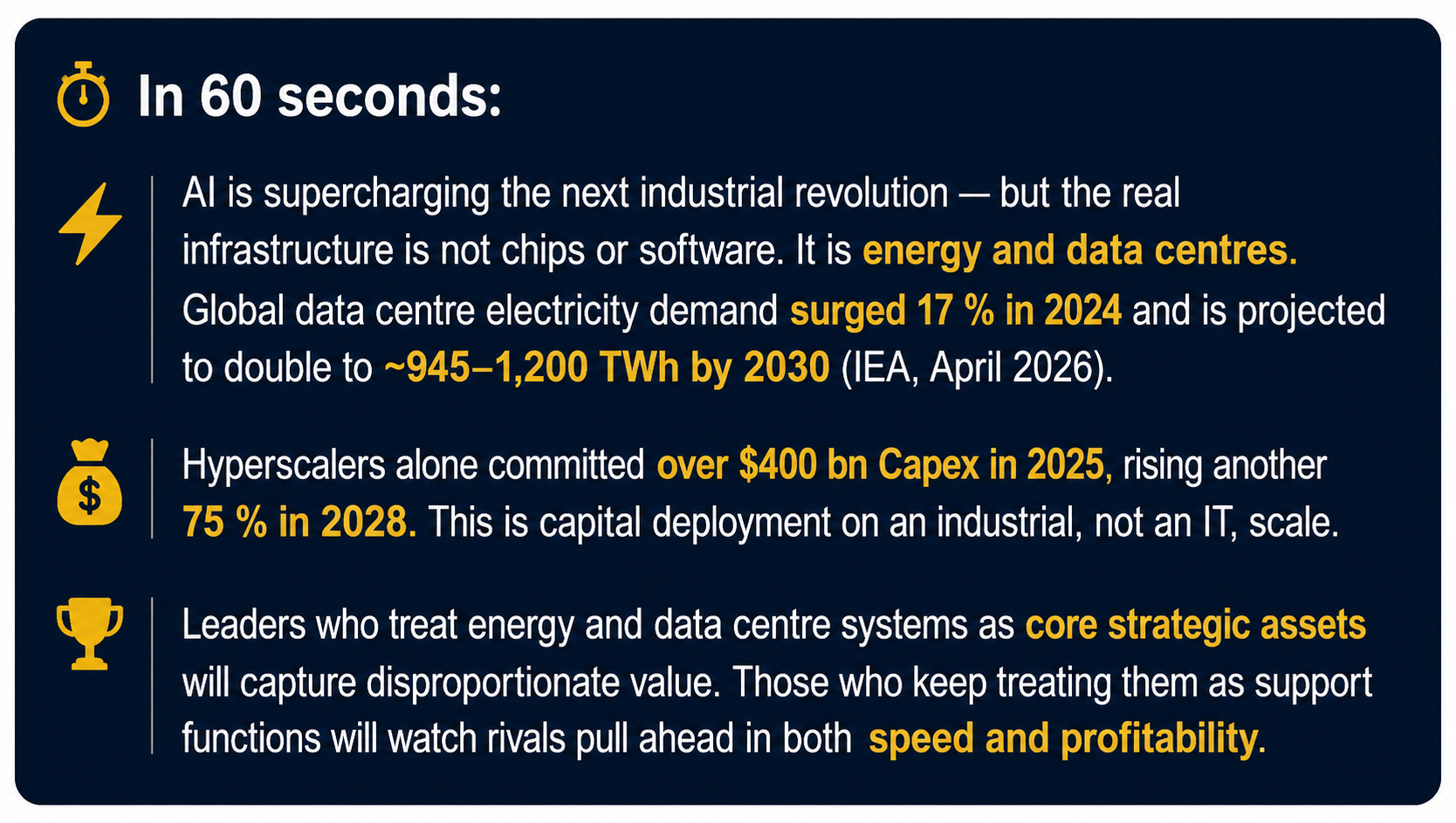

1. The Scale of the Next Industrial Shift

AI is not an incremental technology upgrade, it is reshaping entire economies the way electricity and the internet did before, and at a comparable scale.

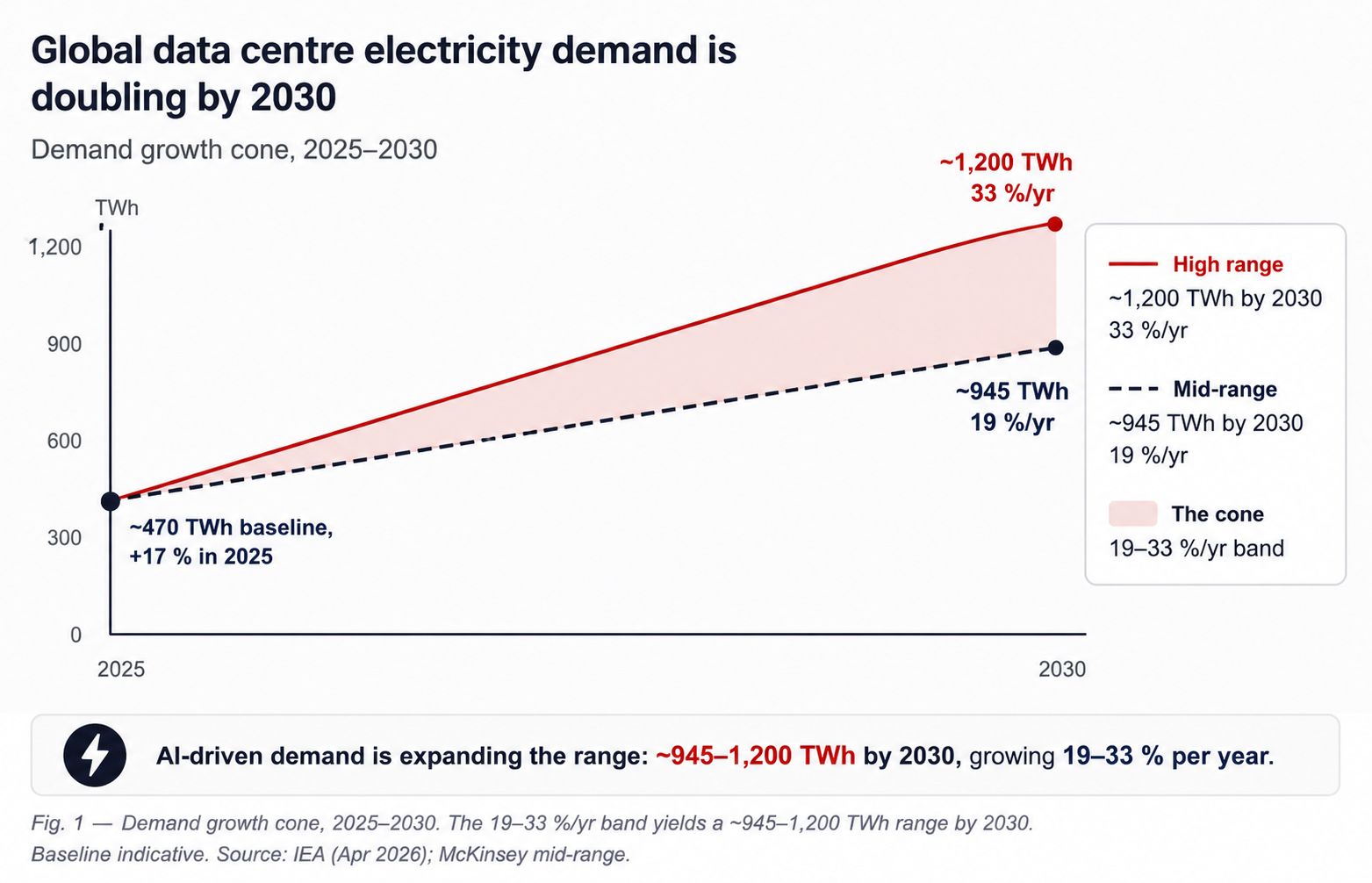

Data centers are becoming the new factories of the information age. Power demand is the binding input: it is growing 19–33 % annually through 2030 in McKinsey's mid-range scenario, and a single hyperscale AI campus can now require 1–5 GW, equivalent to powering entire cities. The capital is moving accordingly: hyperscalers committed over $400 bn in 2025, rising another 75 % in 2026.

Under that growth band, data centre electricity demand roughly doubles to a 945–1,200 TWh range by 2030. The spread between the low and high cases alone exceeds the total demand of many national grids.

👉 Key Insight: This is not a tech story. It is an energy-and-infrastructure story on an industrial scale, and it should be read off the same page as power-plant build-outs, not software roadmaps.

2. Why Energy and Data Centers Are the Deciding Factors

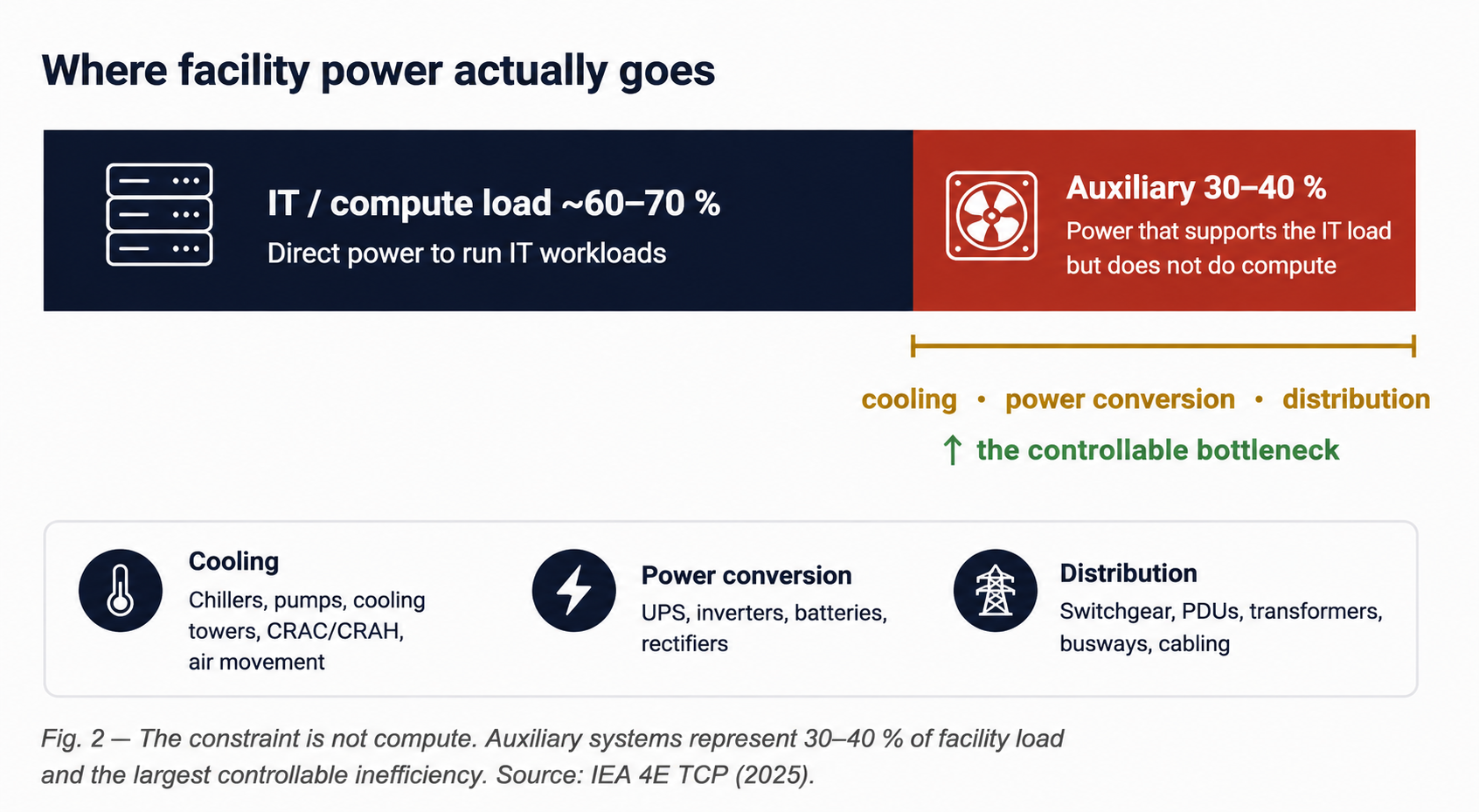

Compute is commoditising. The chips will not be the moat. The power, and the waste around it, will be.

As raw compute becomes a purchasable commodity, the binding constraints shift to power availability, grid interconnection, cooling and auxiliary energy waste, which runs at 30–40 % of facility load in most installations. Procurement-only responses (more PPAs, more offsets) cannot keep pace with absolute demand growth; the result is delay, higher cost and stranded investment.

Operators who optimise system-level efficiency first, liquid cooling, variable-speed drives, integrated power design, unlock faster deployment, lower TCO and genuine emissions cuts. It is the Efficiency Before Fuel principle, carried out of the engine room and into the AI era.

👉 Key Insight: When everyone can buy the same chips, the winner is decided by who wastes the least energy and secures power fastest. The moat moved from silicon to systems.

3. Quantified Scenarios: Who Wins the Industrial Shift

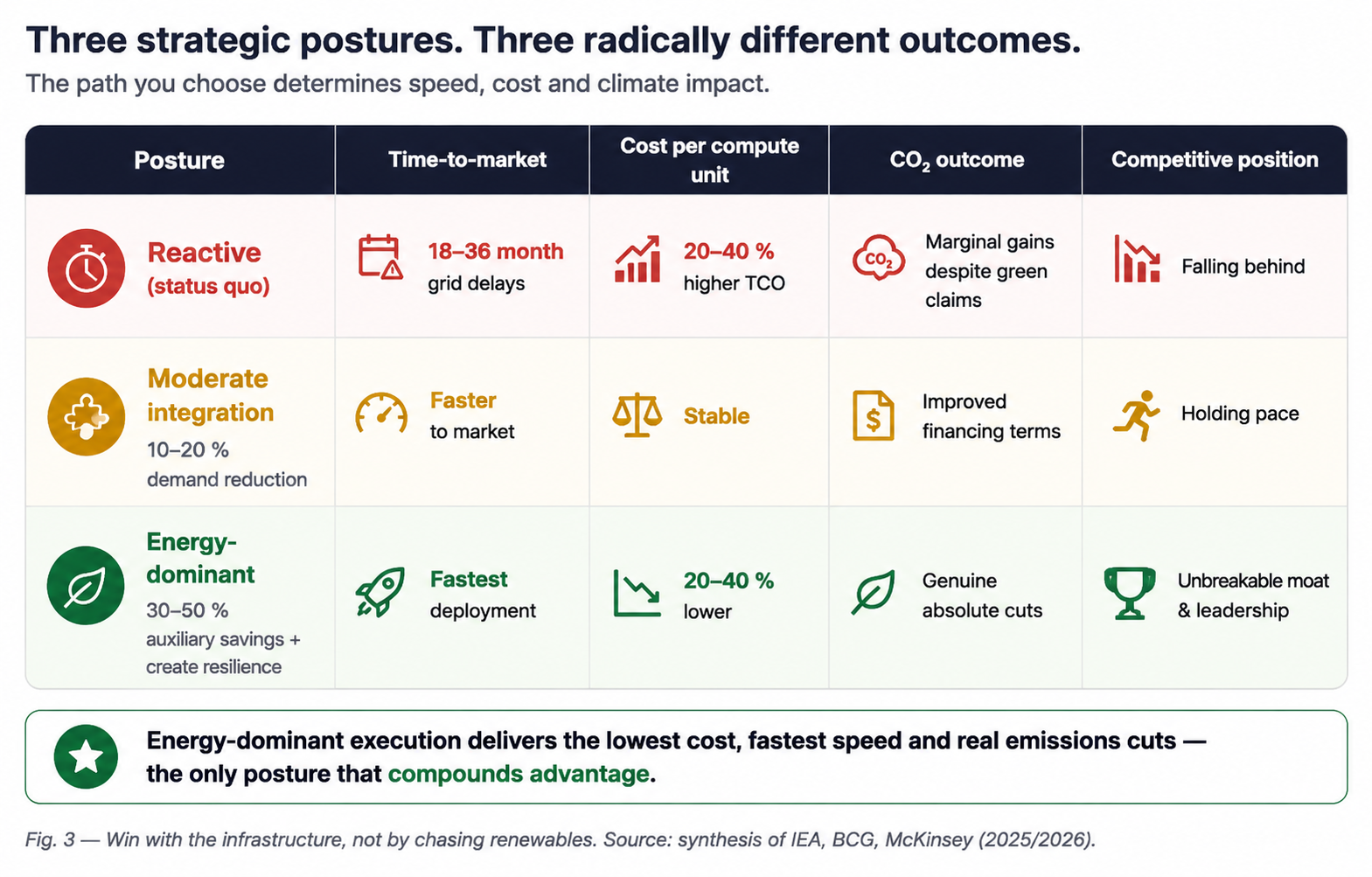

Three postures, three outcomes, and only one builds a durable lead.

Position in the new industrial economy is set by how much demand you remove and how much resilience you own, not by how much green energy you announce.

Modelled across the cited IEA, BCG and McKinsey ranges:

👉 Key Insight: The energy-dominant posture is the only one that compounds, lower cost per compute funds faster deployment, which widens the lead, which lowers cost again. That loop is the moat.

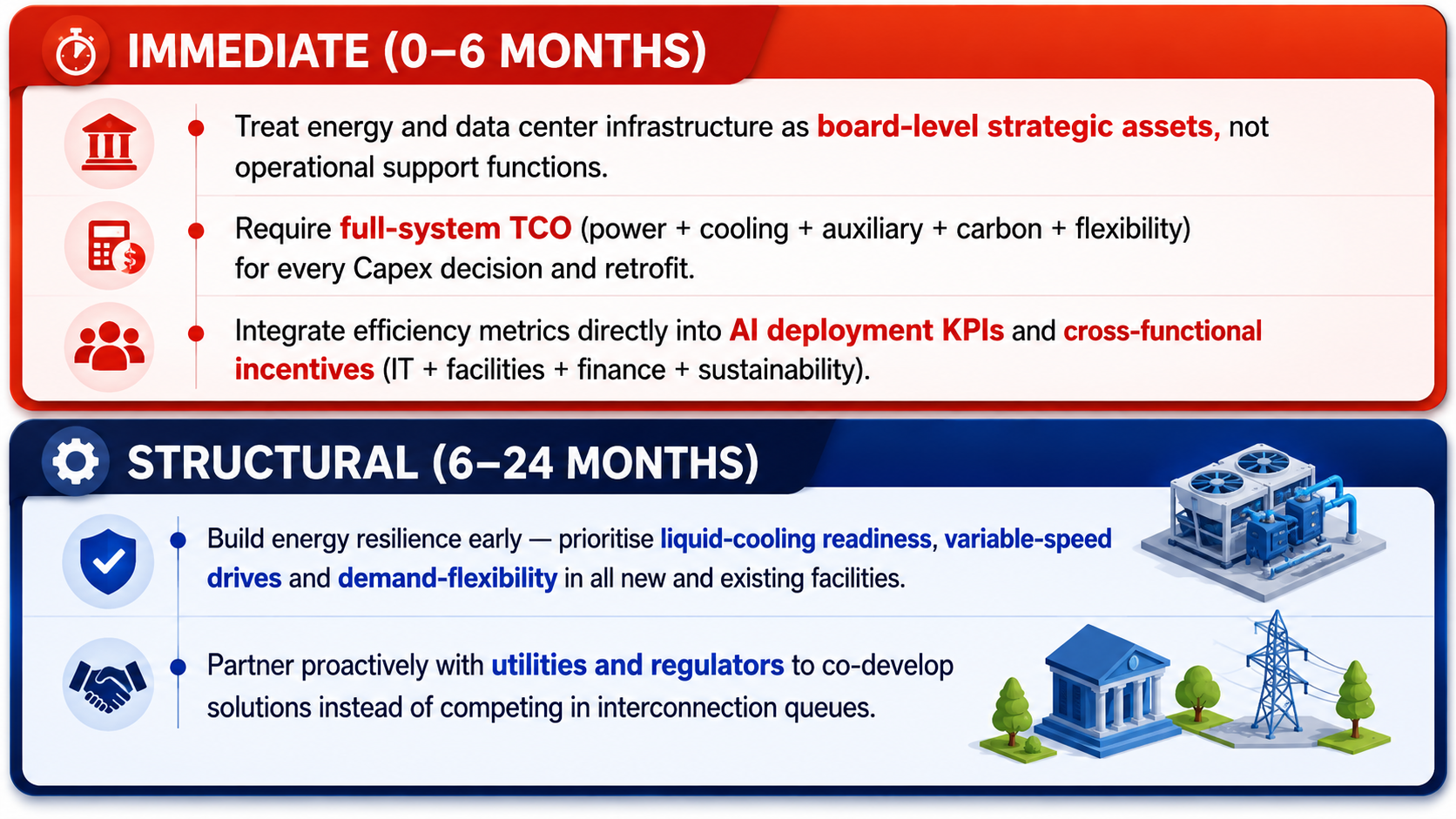

ACTIONS

BOARD CHECKLIST

FINAL THOUGHT

Every industrial revolution has rewarded the same thing: not the most spectacular invention, but the deepest mastery of the infrastructure beneath it. The AI era will be no kinder to the companies that mistake the model for the moat. Energy is the raw material; the data center is the factory; efficiency is the margin. The boards that internalise this ,and act on it before the interconnection queue closes, will own the decade. The rest will rent it. Systems don't fail. Decisions do.

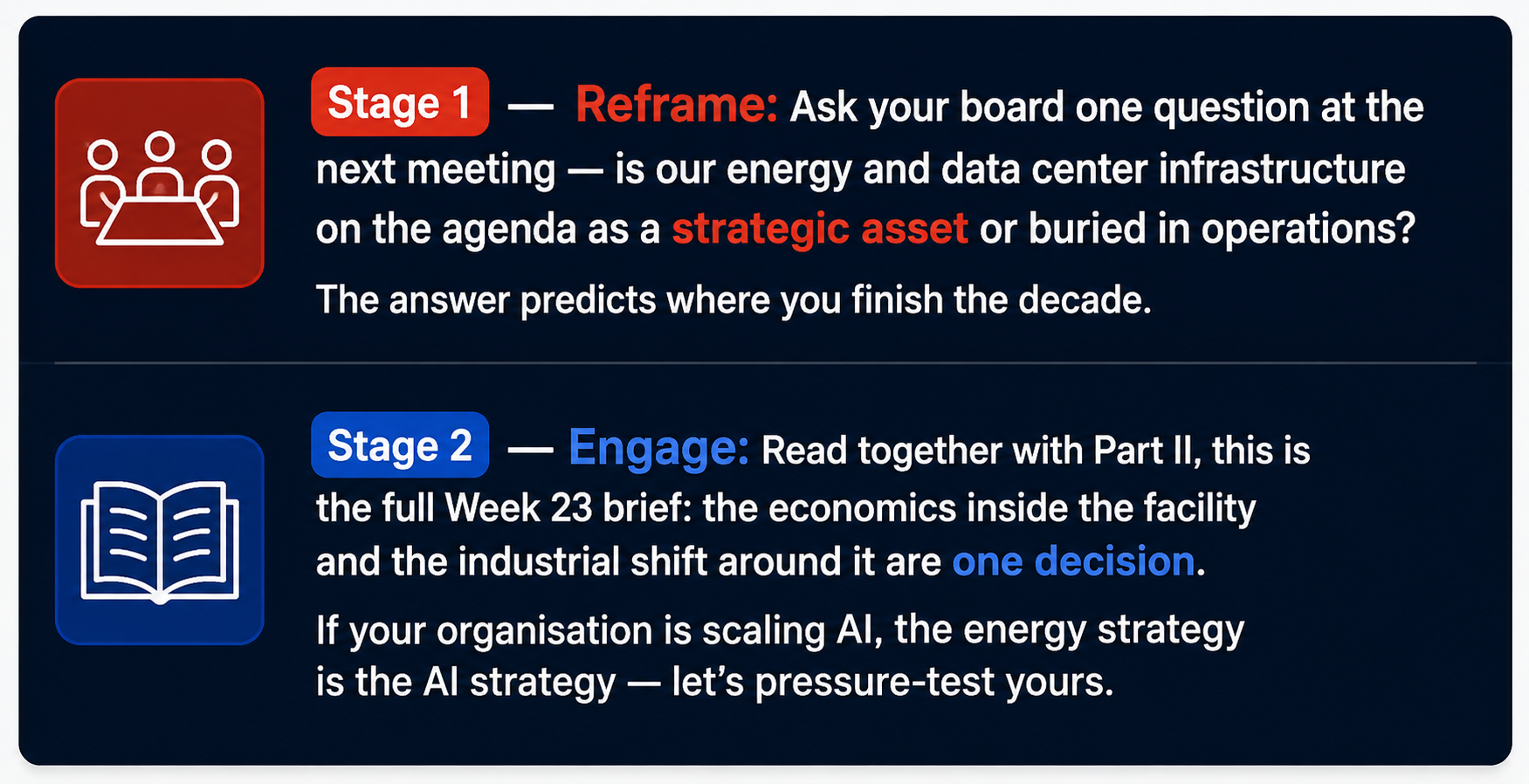

CALL TO ACTION

Take the Next Step

Subscribe to the Weekly Punch for weekly strategic clarity, direct to your inbox.

REFERENCES

International Energy Agency (2026) ‘Data centre electricity use surged in 2025'. Paris: IEA, April 2026.

International Energy Agency (2025) Energy and AI. Paris: IEA.

McKinsey & Company (2025) AI Power: Expanding Data Center Capacity to Meet Growing Demand. New York: McKinsey & Company.

Boston Consulting Group (2025) Breaking Barriers to Data Center Growth. Boston: BCG.

IEA 4E Technology Collaboration Programme (2025) Data Centre Energy Use: Critical Review of Models and Results. Paris: IEA 4E TCP, March 2025.

Note: This article reflects my personalviews based on industry experience and publicly available information. It does not constitute professional, legal, or investment advice and does not represent the views of my employer. AI-generated visuals, concept and content by the author.