The Leadership Gap in AI Data Center Decisions

ENERGY DOMINANCE SERIES · WEEK 21 · PART II

Why C-Level Risk Aversion and Short-Term KPIs Are Blocking the Next Wave of AI Dominance

AI INFRASTRUCTURE | LEADERSHIP & CULTURE | May 2026

Part I established that energy is the primary rate-limiter on AI deployment. Part II addresses the deeper question: why do most organisations fail to act on that fact? The infrastructure is available. The economics are proven. The data is published. What remains is the decision, made in a boardroom, not a server hall. In 2026, energy inefficiency in AI infrastructure carries a C-suite signature. Every quarter it goes unaddressed is a quarter of competitive advantage transferred to someone else.

EXECUTIVE SUMMARY

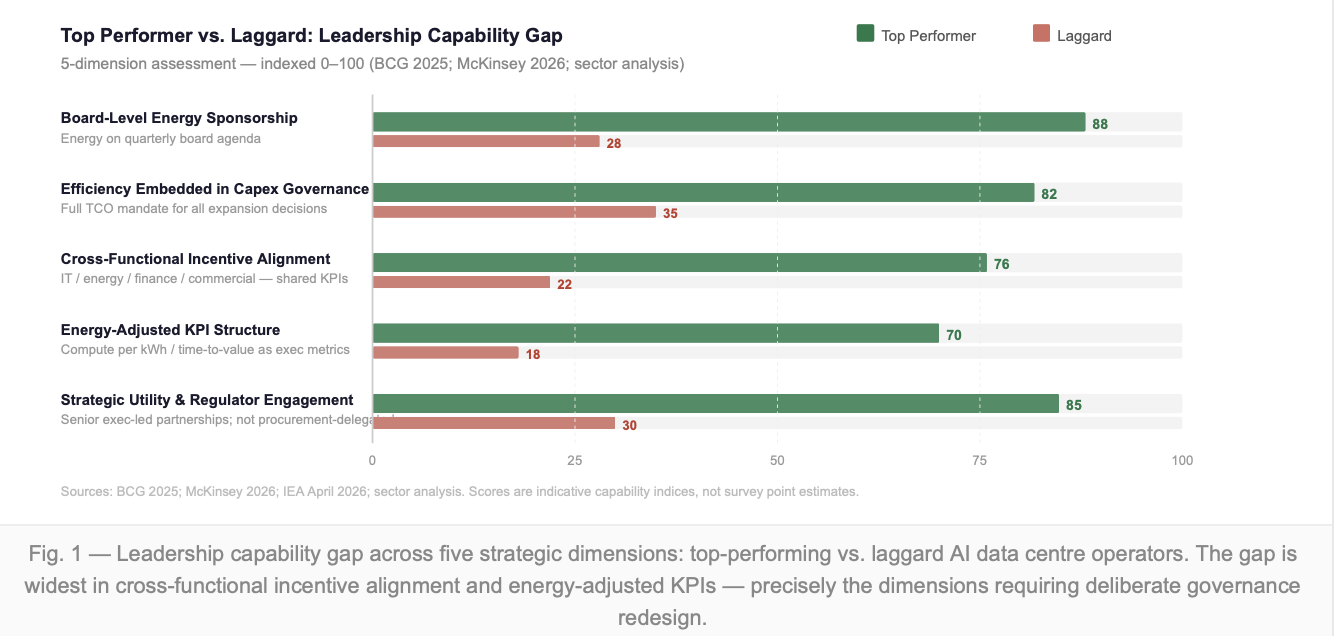

The Leadership Gap in Numbers

The performance divergence between top-performing and laggard AI data centre operators is now documented with sufficient granularity to be unambiguous. BCG's 2025 analysis and McKinsey's March 2026 data identify a consistent pattern: operators who secure board-level energy sponsorship, integrate efficiency into Capex governance and structure cross-functional accountability consistently outperform those who do not, across every measurable dimension of deployment speed, cost and capital efficiency.

The gap is not marginal. Organisations with strong executive energy leadership achieve 15–30 % lower TCO through proven system-level measures, VFD, liquid cooling, high-efficiency power delivery, that laggards consistently under-invest in. They access better financing terms because lenders now price energy risk explicitly. They secure permitting faster because they engage regulators as strategic partners. The performance differential compounds annually as grid congestion intensifies and carbon costs escalate.

In 2026, energy inefficiency in AI infrastructure is no longer a technical issue. It is a leadership and culture issue, and every dimension of the capability gap is within the direct control of the C-suite.

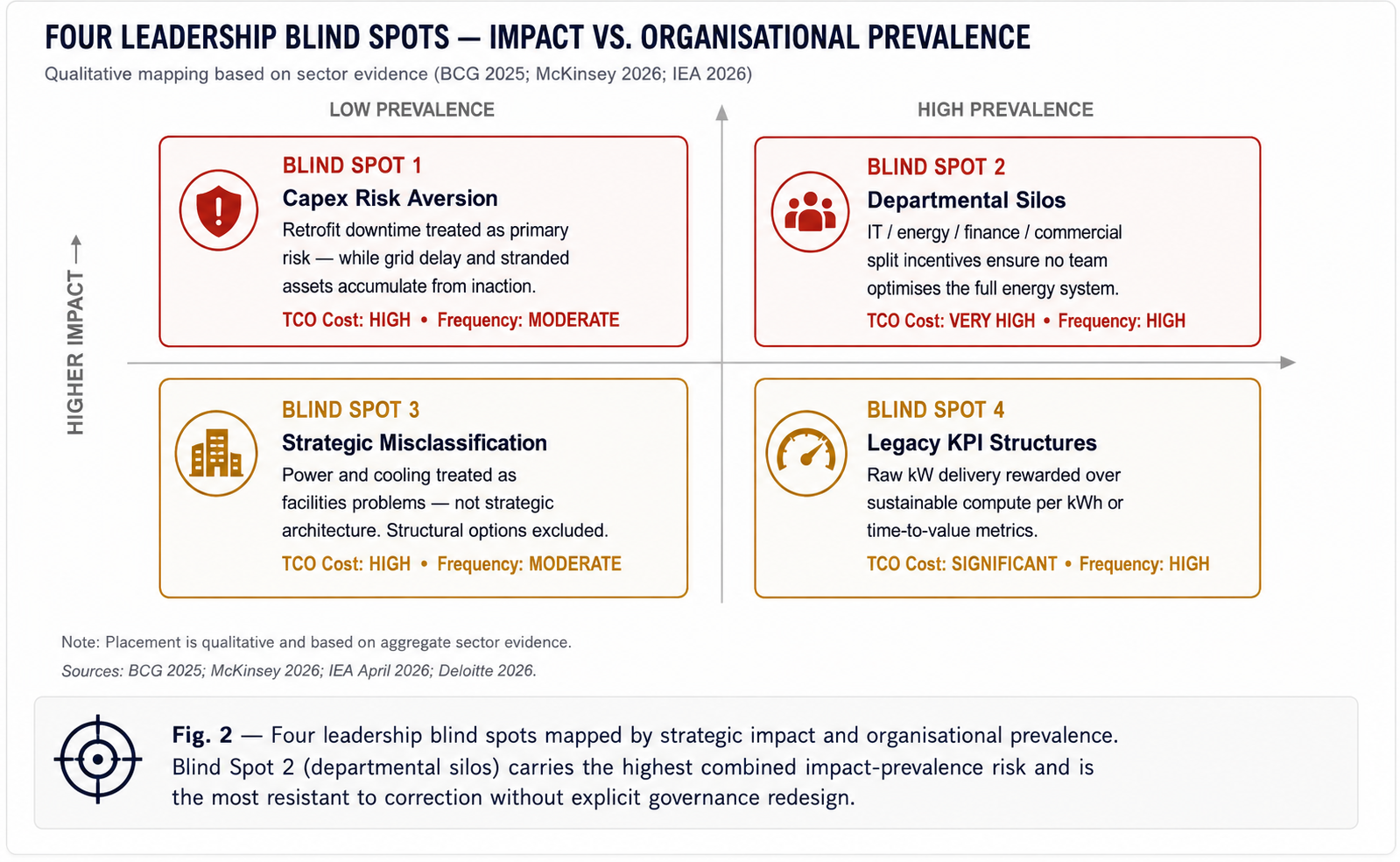

The Four Leadership Blind Spots

Across the AI data centre sector, four structural patterns of leadership failure recur with sufficient consistency to constitute a taxonomy. Each is individually costly. In combination, they produce the compounding disadvantage that separates laggard operators from those building genuine energy moats.

The first is systematic misclassification: treating power and cooling as facilities engineering problems rather than core strategic architecture decisions. This framing confines the solution space to procurement and operational efficiency, excluding the structural options, onsite generation, demand flexibility, system-level redesign, that produce durable advantage. The second is Capex risk aversion: treating retrofit downtime and capital outlay as primary risks while systematically underweighting grid delay, stranded assets and regulatory exposure that accrue from inaction. Third, legacy KPI structures reward raw scale, megawatts brought online, rack density, utilisation rate, without reference to the energy cost and carbon intensity of that scale. The fourth blind spot is the most institutionally entrenched: departmental silos between IT, energy, finance and commercial teams that mirror the split-incentive failures that destroyed capital efficiency in conventional industries. When energy cost sits in facilities, deployment timeline sits in IT and Capex approval sits in finance, no single team has the mandate, or the metrics, to optimise the system.

The four blind spots share a common root: treating energy as a cost to be managed rather than a system to be architected. Fixing one blind spot without addressing the governance root leaves the others intact.

Real-World Evidence from 2025–2026

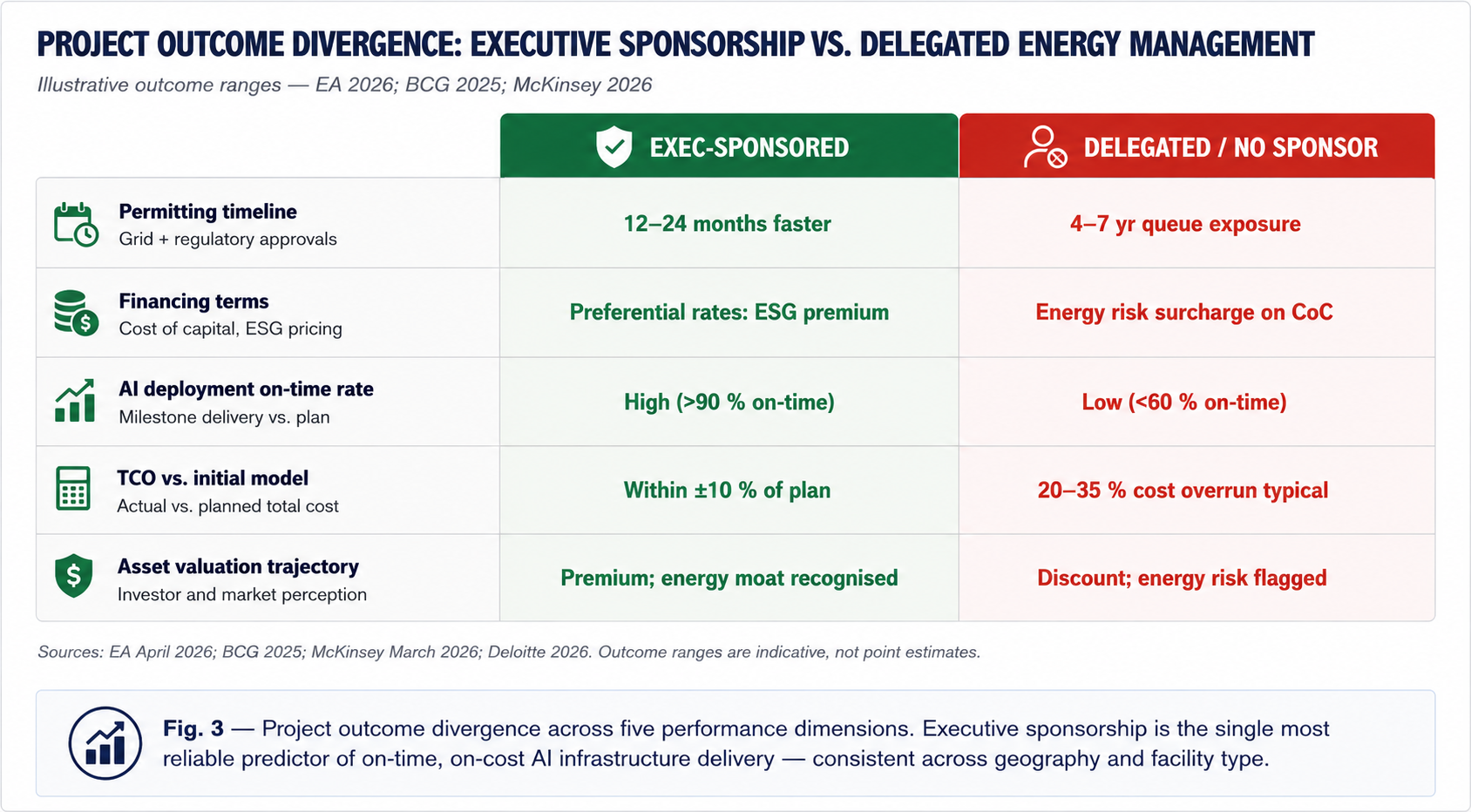

The performance differentiation is now visible in published data. IEA's April 2026 report and analyses from BCG and McKinsey identify a consistent pattern: projects with strong executive sponsorship for energy optimisation, where the CEO or board has personally endorsed energy as a strategic deployment priority, consistently achieve faster permitting, better financing terms and materially higher on-time delivery rates for AI deployment milestones.

The contrast with laggard projects is stark. Projects without executive sponsorship follow a predictable sequence: facilities teams propose efficiency investments that finance defers on Capex grounds; grid delays materialise that were foreseeable with better energy intelligence; retrofit projects stall because no single executive owns the outcome; regulators are engaged reactively, after approvals are already delayed. The result is not merely higher operational cost, it is compressing competitive positioning into quarterly reports as write-downs, missed timelines and financing cost surcharges.

Executive sponsorship is not a soft governance preference, it is the single most reliable predictor of on-time, on-cost AI infrastructure delivery. The evidence is now consistent enough to be used as an underwriting criterion by lenders and institutional investors.

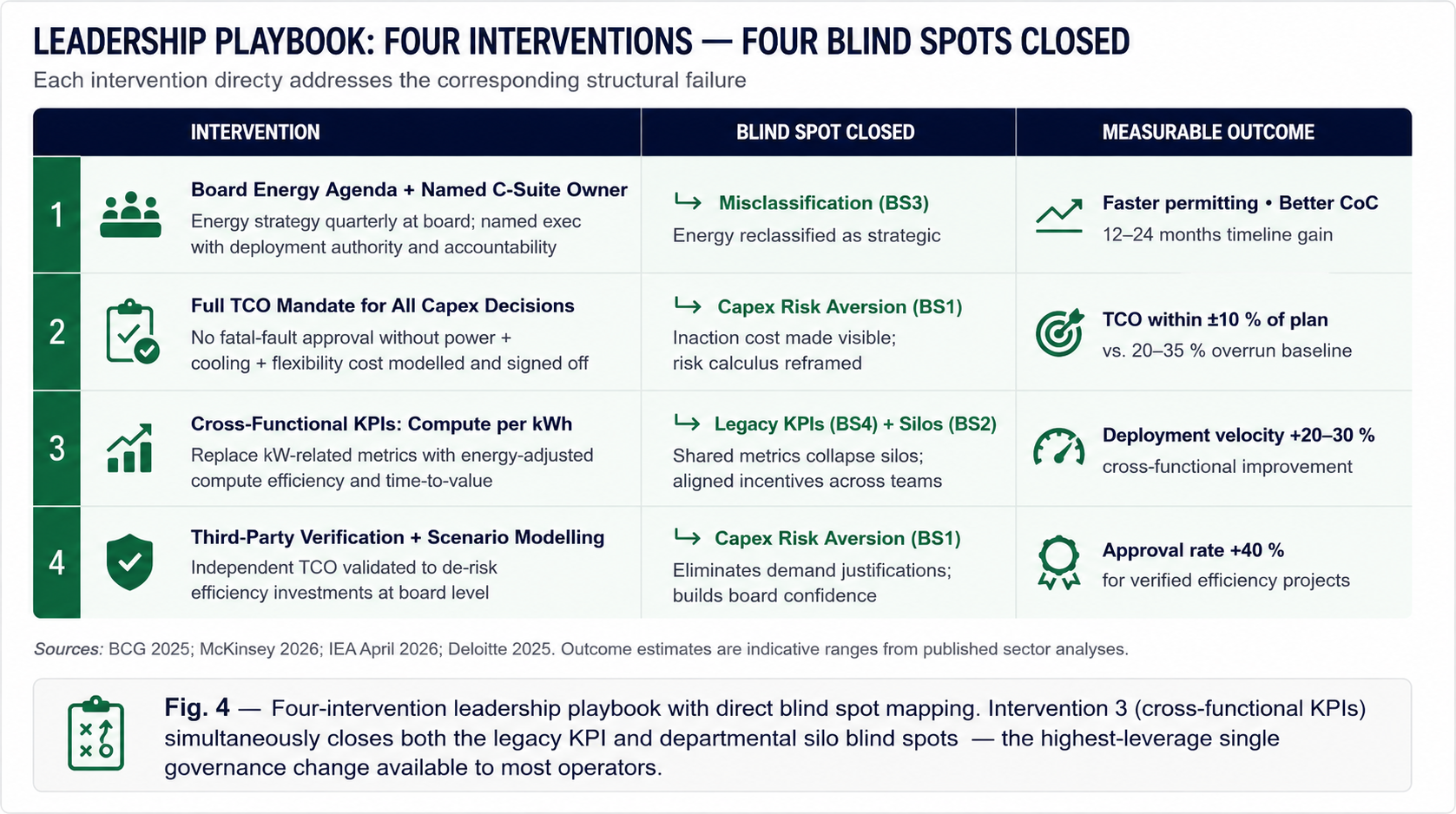

The New Leadership Playbook for AI Energy Dominance

Closing the leadership gap requires four deliberate governance interventions, each targeting one of the structural blind spots identified in Section 2. These are not aspirational principles. They are specific, implementable changes to decision rights, metrics and accountability structures that leading operators are executing now.

The playbook is not complex. Each intervention is established practice in adjacent industries. The barrier is not knowledge, it is the organisational will to redesign governance structures built for a world where energy was cheap, abundant and competitively irrelevant. That world no longer exists.

ACTION RECOMMENDATIONS

MMEDIATE ACTIONS: THIS WEEK

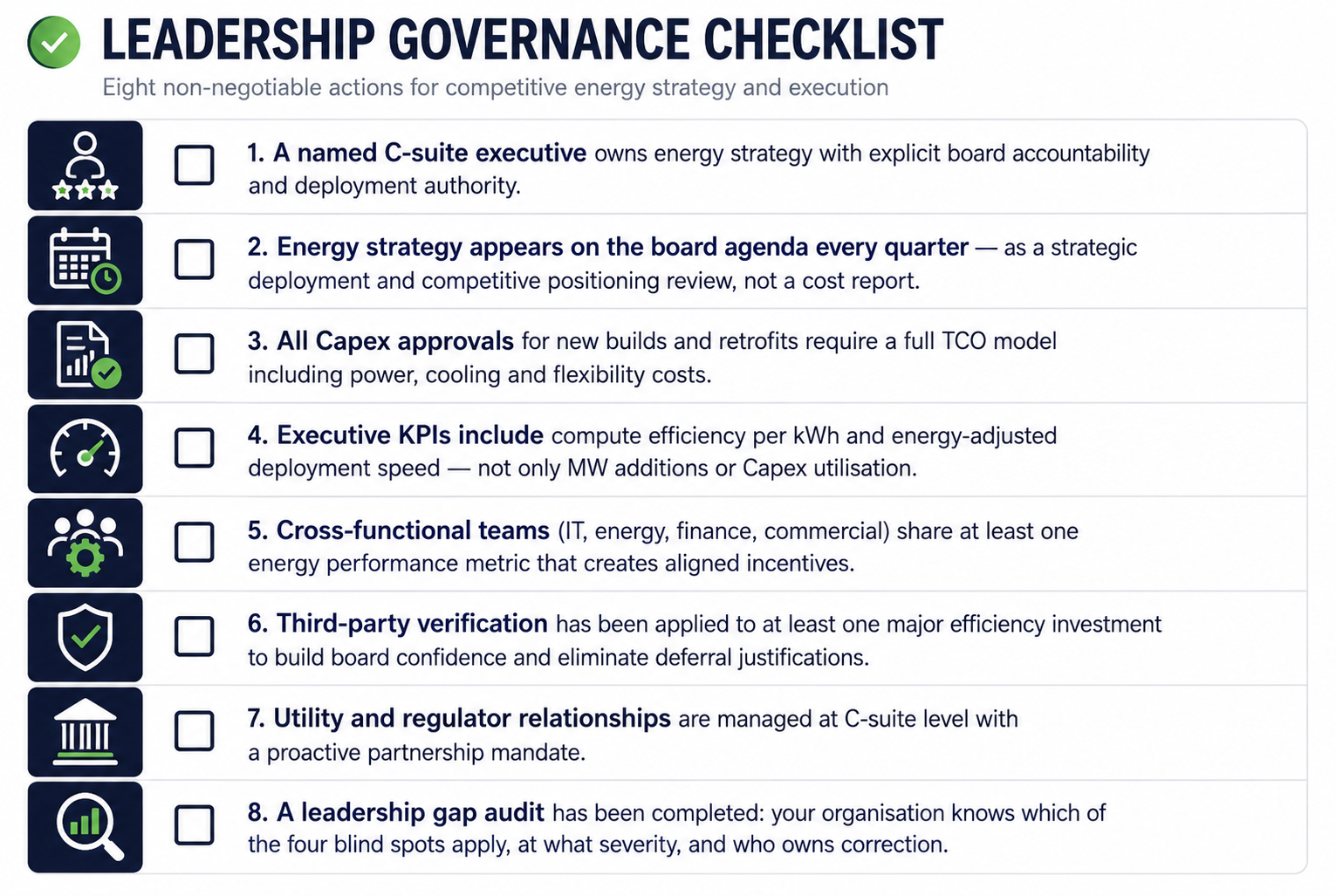

Name a C-suite owner for energy strategy, not a VP of Facilities. This single decision changes the organisational framing of every subsequent energy discussion.

Audit your current KPI architecture: identify every metric that rewards MW delivery or Capex avoidance without reference to energy efficiency or deployment speed.

Commission third-party scenario modelling for your two highest-priority expansion decisions, before the next Capex approval cycle.

6–24 MONTH STRATEGIC COMMITMENTS

Put energy strategy on the board agenda every quarter, with a standing report covering TCO performance, deployment timeline exposure and energy sovereignty progress.

Redesign cross-functional KPIs across IT, energy, finance and commercial to include shared energy efficiency and deployment velocity metrics.

Mandate full system TCO (power + cooling + flexibility) as a prerequisite for all new build and retrofit Capex approvals from Q3 2026 forward.

Elevate utility and regulator engagement to senior executive level, with the explicit objective of co-creating solutions rather than seeking approvals reactively.

LEADERSHIP CHECKLIST: CLOSING THE GAP

The technology is ready. The economics are proven. The data is published. What remains is the decision, made in a boardroom, not a server hall, to treat energy as the competitive weapon it has already become. Every organisation that defers that decision is not managing risk. It is accumulating it, quarter by quarter, in the form of deployment delays, stranded Capex and widening competitive gaps that compound with every year the grid stays congested. The leadership gap is closeable. The question is whether it gets closed by design, or by the discipline of falling behind.

Energy Dominance Series-Week 21, Part II of II.

Together, Parts I and II constitute the complete Week 21 strategic brief: the energy moat thesis and the leadership decisions required to build it. Week 22 moves to implementation mechanics, VFD economics, liquid cooling retrofit ROI and procurement frameworks for firm power.

Take the Next Step

Subscribe to the Weekly Punch for weekly strategic clarity, direct to your inbox.

REFERENCES

BCG (2025). Breaking Barriers to Data Center Growth. Boston Consulting Group. Available at: bcg.com [Accessed May 2026].

Deloitte (2025). AI Infrastructure Leadership Survey. Deloitte Insights, 2025. Available at: deloitte.com [Accessed May 2026].

IEA (2026). Key Questions on Energy and AI. International Energy Agency, April 2026. Available at: iea.org [Accessed May 2026].

McKinsey & Company (2026). The $7 Trillion Race for AI Data Center Infrastructure. McKinsey Global Institute, March 2026. Available at: mckinsey.com [Accessed May 2026].

Note: This article reflects my personalviews based on industry experience and publicly available information. It does not constitute professional, legal, or investment advice and does not represent the views of my employer.