Critical Minerals & Rare Earths:The Invisible Chokepoint Killing AI and Manufacturing

Geopolitics · Supply Chain · Critical Minerals · AI & Manufacturing

EXECUTIVE SUMMARY

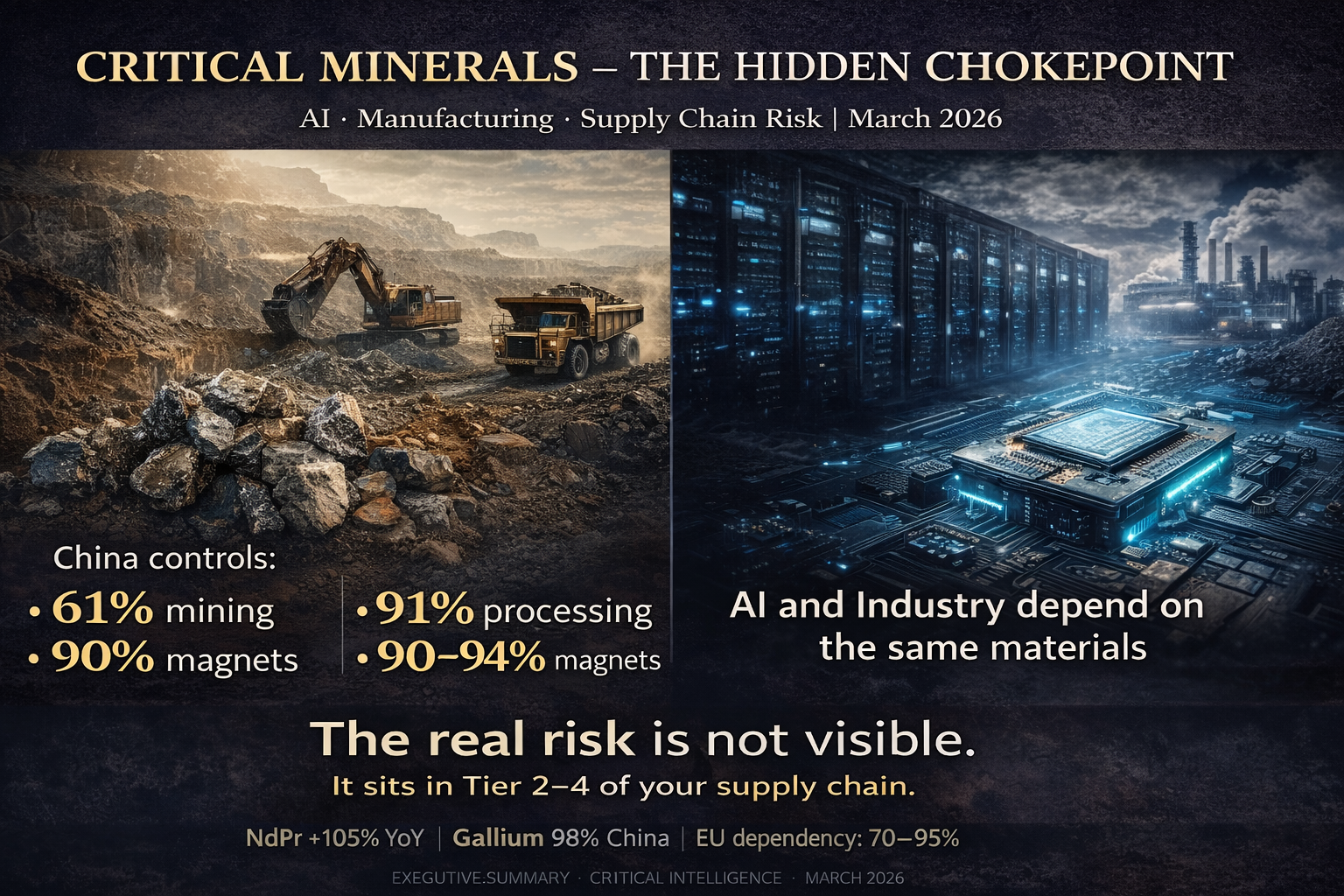

While the debate continues over Hormuz-driven energy shocks, the next — and more dangerous — black swan is already forming: Critical Minerals and Rare Earths. China controls approximately 61% of global mining output, 91% of processing capacity, and 90–94% of permanent magnet production in 2026. Export controls introduced in 2025 have already triggered price spikes and delivery bottlenecks. At the same time, demand is exploding through AI data centres, electric motors, and energy-efficient industrial systems.

Key empirical findings:

NdPr oxide prices (neodymium-praseodymium) reached 108–117 USD/kg in March 2026 — up to +105% year-on-year (S&P Global, 2026)

The EU imports 70–95% of its rare earths from China — even when sourced via third countries, the raw material typically originates from Chinese processing (IEA, 2025)

Gallium (98% from China) and germanium are essential for high-performance AI chips — without them, no agentic AI, no photonic computing (USGS, 2026)

65% probability of new licence delays or selective export restrictions by June 2026, particularly for defence and AI end-use applications

Companies with active resilience systems secure a 90-day buffer — the rest pay 15–25% higher component costs or are forced to halt projects

Three conditions for resilience:

Full transparency over your critical mineral exposure — at least four supply chain tiers deep

Dual-sourcing as a system, not a slide — with two complete value chains and an active recycling loop

CEO-level ownership: without executive sponsorship, diversification remains a presentation

This article explains the evidence, the mechanisms, and what executives must do now.

1. NWC Is a Survival Metric — Critical Minerals Are Its Silent Killer

Systems don't fail. Decisions do.

Most companies do not lose their competitive position through a single dramatic event. They lose it through structural blindness to risks that have been building for years. Critical minerals are the textbook example of this mechanism: they are embedded in virtually every modern industrial component — from electric motors and pumps to semiconductors — and yet most supply chain analyses simply fail to ask the right questions.

Net Working Capital (NWC) is the first instrument to register this pressure: when raw material costs rise, lead times extend, and safety buffers must be built, the impact shows up directly in Inventory Days, Days Sales Outstanding, and the Cash Conversion Cycle. The problem is that most organisations only notice when liquidity is already under strain.

Hofmann (2010) demonstrates across a sample of more than 7,000 firms that working capital efficiency did not structurally improve over time — because improvements were often redistributions, not genuine optimisations. The same logic applies to raw material risk: adding a second supplier to a shortlist achieves nothing if both draw from the same Chinese processor.

👉 Critical minerals are not a commodity topic. They are the new structural chokepoint for manufacturing and AI roadmaps.

2. China's Control Is Not a Risk — It Is a Geopolitical Weapon

The 2026 figures are unambiguous: China controls 61% of global rare earth mining, 91% of processing capacity, and 90–94% of neodymium-iron-boron (NdFeB) magnet production — the most powerful permanent magnets used in electric motors, generators, loudspeaker systems, and cooling pumps for data centres (USGS, 2026).

In 2025, China actively deployed this position as leverage: export licences were introduced for seven heavy rare earths — including dysprosium and terbium, which are indispensable for high-temperature-stable magnets. Export bans on magnet production equipment followed, with an explicit prohibition on defence end-use. Parts of these measures were suspended until November 2026 — not lifted. The structural lever remains firmly in place.

Bloomberg Intelligence (2026) forecasts that China's market share could decline to approximately 69% by 2030. But this is a gradual shift — it offers no short-term solution for companies that need to source components today. S&P Global (2026) confirms: supply bottlenecks will persist through 2026, and price volatility remains structurally embedded.

This hits European mid-market manufacturers particularly hard: the EU imports 70–95% of its rare earths from China. Even when the transit country is Malaysia, Vietnam, or Japan, the raw material in most cases originates from Chinese beneficiation or contains Chinese-processed concentrate (IEA, 2025). Reuters (2025) describes the dilemma precisely: the West is attempting to close the gap, but alternative processing capacity will not be available before 2028–2030.

👉 Companies that stop their supply chain analysis at Tier-1 systematically — and structurally — underestimate their exposure.

3. The AI Boom Amplifies Every Bottleneck — Not Just Power Demand

Public debate on AI infrastructure focuses on electricity demand and compute capacity. That is correct — but incomplete. A single hyperscale data centre does not only require megawatts. It also requires:

Gallium and germanium for high-performance semiconductors (GaN chips, SiGe transistors) — 98% of global gallium supply originates in China (USGS, 2026)

NdFeB magnets for thousands of cooling pumps, fan motors, and rack systems — directly dependent on Chinese magnet production

Dysprosium and terbium for thermally stable magnets in high-performance environments — sourced exclusively from Chinese-controlled processing

Indium and telluride for display and sensor technologies in server hardware — equally concentrated supply chains

This means: any company seeking to optimise its production lines with agentic AI, digitalise its pump and motor systems, or steer logistics through machine learning is exposed twice — once through the direct mineral requirements of its physical products, and once through the critical mineral dependency of the AI infrastructure itself.

The price dynamic amplifies this effect: NdPr oxide traded between 108 and 117 USD/kg in March 2026 — up to 105% above the prior-year level (S&P Global, 2026). For manufacturers of electric motors, pumps, or drive systems, this translates directly into component cost increases of 30–50%, with little ability to pass them through in competitive markets.

👉 AI scaling and physical manufacturing are competing for the same scarce materials. Ignoring this means planning on sand.

4. Disruption Is No Longer the Exception — It Is the Operating Mode

Analysing the last five years reveals a consistent pattern: supply chain disruption is no longer the tail-risk scenario in risk assessments. It has become the structural operating mode of global value chains.

2021: the semiconductor shock. 2022: the gas and energy shock. 2024: escalating Taiwan Strait tensions. 2025: rare earth export control escalation. 2026: the Hormuz shadow and further mineral restrictions simultaneously. The mechanism is consistent: when external shocks meet structurally vulnerable supply chains, the damage multiplies.

Wetzel and Hofmann (2019) have empirically substantiated this dynamic: companies with financially fragile supplier partners are forced to extend their Cash Conversion Cycle by 29–35 days when external shocks hit — because suppliers tighten payment terms and safety stocks must be built up. The critical point: forcing aggressive NWC targets onto fragile networks does not create performance. It creates instability.

For critical minerals, the same principle applies in an intensified form: a single bottleneck in NdFeB magnets can paralyse global supply chains, because few European manufacturers hold more than 90 days of buffer stock and alternatives are not rapidly available. The USGS (2026) confirms: substitution options for critical magnets are technically limited and economically non-scalable for years.

👉 Companies that treat resilience as a cost factor have misunderstood the question. Resilience is the price of operational capability.

5. The 5-Phase Ownership System: From Slide Deck to Execution

Diversification as a slide already exists in most companies. What is missing is diversification as a system — embedded in processes, accountability structures, and measurable KPIs. The following framework is not a theoretical construct. It has been developed through practical work on AI-driven sales and supply chain collaboration, directly adapted to the critical mineral challenge.

Phase 1 – Visibility: You Cannot Manage What You Cannot See

The first step is uncomfortable: a full critical mineral exposure analysis, at least four supply tiers deep. Not just direct suppliers — but their suppliers, their raw material sources, and their processing partners. The goal is an AI-driven risk dashboard with an automated scorecard that displays, for each relevant component: raw material origin, processing country, geopolitical risk index, and substitution feasibility.

Concretely: if an NdFeB magnet in a pump carries 94% China exposure, that must be visible — not in an annual report, but in real time on an operational dashboard updated weekly.

Phase 2 – Dual-Sourcing as a Complete Value Chain

Dual-sourcing does not mean two suppliers on a list. It means two complete, independent value chains. For rare earths, this translates concretely into: an Australian-Vietnamese sourcing route (MP Materials, Lynas) combined with an active recycling loop for end-of-life magnets from your own product portfolio.

Target by 2028: below 65% dependence on a single country for each critical material. This threshold is not arbitrary — it represents the point at which alternative sourcing capacity can realistically bridge a 90-day primary supply disruption (IEA, 2025).

Phase 3 – Circular Ownership: Your Products as a Raw Material Source

The most advanced form of resilience is closing the loop: in-house magnet recycling programmes, partnerships under EU Strategic Projects within the Critical Raw Materials Act (CRMA 2024) and RESourceEU (2025), and the development of closed-loop assets from your own product base.

Specifically for pump and motor manufacturers: a take-back programme for used units, combined with a certified recycling partner, reduces primary raw material dependency by 10–20% in the medium term — while simultaneously building a sustainability narrative for ESG reporting and customer relationships. The European Commission (2025) is actively funding exactly these approaches through the RESourceEU programme.

Phase 4 – Human Judgment Loop: Weekly Ownership Decisions

Technology creates visibility. Humans make decisions. The critical link is missing in most organisations: a structured, weekly process in which sales and supply chain jointly make ownership decisions — not via email, not in quarterly reviews, but in a fixed 30-minute ritual with a clear accountability matrix.

This format — weekly, structured, decision-oriented — is the core of the AI-supported sales and supply chain collaboration model developed from practitioner experience. It prevents raw material risks from disappearing into functional silos and only reaching the CEO when it is too late.

Phase 5 – Measure & Iterate: If You Don't Measure It, You Lose It

The final element of the system is the monthly KPI set. Three core metrics are non-negotiable:

China exposure in %: the share of each critical raw material sourced — directly or indirectly — from Chinese-controlled mining or processing

Hedging effectiveness: variance between actual procurement costs and planned costs for critical minerals — an indicator of hedging strategy performance

Productivity gain from supply stability: ratio of unplanned production stoppages (mineral-related) to total production time — a direct resilience indicator

👉 This is not a project. It is Ownership as Design — a structural decision about how an organisation responds to systemic risk.

6. The 3-Month Outlook: What April to June 2026 Will Bring

Forecasting in geopolitically charged commodity markets is notoriously difficult. Nevertheless, available data allows a structured assessment — with explicit probabilities:

Prices (high confidence): NdPr and dysprosium will remain 20–40% above 2025 levels. Gallium and germanium remain volatile with swings of ±25%, depending on Chinese quarterly export licence decisions

Supply risk (65% probability): new licence delays or selective restrictions, particularly for defence and AI end-use applications. The lever remains — only the intensity of its use is uncertain

EU progress (structurally limited): RESourceEU and CRMA projects are progressing, but new processing capacity will not come online before 2028–2030. By June 2026, realistically only +5–8% diversification of available non-China sources

Winners vs. losers (clear bifurcation): companies with an active 5-phase system secure a 90-day buffer and win contracts because they can deliver. The rest pay 15–25% higher component costs — or are forced to halt projects

👉 The window for proactive action is closing. Companies that move now gain a structural lead of 12–18 months over those that wait.

7. What to Do — Now and Strategically

Abstract recommendations serve no one. The following distinction is deliberate: what is actionable this week — and what requires a 24-month commitment?

Immediate actions (this week)

Launch a critical mineral audit: which components in your portfolio contain NdFeB magnets, gallium-based semiconductors, or other controlled materials? Analyse at least four tiers deep — not just Tier-1

Quantify China exposure: for each identified component, calculate the percentage of raw material sourced from Chinese-controlled origins. Prioritise components with >70% exposure

Assess the financial health of key suppliers: financially stretched suppliers are the first to fail when commodity shocks hit — this must be factored into NWC planning

Strategic commitments (6–24 months)

Establish CEO-level ownership: critical minerals span procurement, production, sales, and finance. Without executive sponsorship, diversification stays a departmental matter — and fails

Build alternative sourcing value chains: evaluate partnerships with Australian and Canadian rare earth producers; deploy supply chain finance instruments to fund inventory build-up

Close a recycling partnership: leverage EU funding programmes under CRMA 2024 and RESourceEU 2025 — the funding is available, and most companies have not yet applied

Build a real-time monitoring technology stack: AI-driven dashboards that integrate commodity prices, delivery status, and geopolitical risk indices — without this tool, the system remains blind

👉 The difference between winners and losers in this cycle is not capital. It is decision speed — and structural preparation.

8. Why Mid-Market Manufacturers Are Most Exposed

Large corporations have critical mineral teams. They hold long-term supply agreements, warehousing capacity, and political access to early warning systems. European mid-market manufacturers have none of these — and yet carry the same exposure.

Wang (2026) analyses this dilemma through an automotive SME case study: the company successfully optimised its Cash Conversion Cycle — and still slid into sustained losses. Root causes: market concentration, weak bargaining power vis-à-vis large customers, and raw material cost pressure that could not be passed through to end markets. Operational efficiency was necessary — but not sufficient.

For mid-market companies in pump manufacturing, drive systems, or specialised machinery, this holds with particular force: they purchase in small volumes, lack commodity hedging instruments, and cannot afford dedicated supply chain finance teams. At the same time, their products — electric motors, pumps, drive systems — are precisely the components with the highest critical mineral intensity.

The solution does not lie in imitating large corporate structures, but in intelligently deploying available levers: purchasing cooperatives with other mid-market firms, shared inventory strategies, consortium participation in EU Strategic Projects, and targeted use of supply chain finance instruments that preserve cash and enable buffer-building.

👉 Operational strength does not protect against structural exposure. Mid-market companies do not need corporate-scale solutions — but they do need corporate-level clarity about their own vulnerability.

Final Thought

Energy was the pain of 2022.

Critical minerals are the game-changer of 2026.

The difference: with gas, everyone knew there was a problem the moment the invoices arrived. With rare earths, many companies will only discover the problem when production lines stop — because a supplier three tiers away can no longer source a magnet.

Companies that build Ownership as Design now do not just gain resilience. They gain market share — because they can deliver when others cannot.

The crisis does not begin when the supply chain breaks. It begins when nobody is watching.

References

Bloomberg Intelligence (2026) World scrambles for rare earths to erode China's dominance from 90% to 69% market share. Bloomberg LP, 2 March.

European Commission (2025) RESourceEU Action Plan. Brussels: European Commission.

Hofmann, E. (2010) Zum Wandel des Working Capital Managements in Supply Chains.

International Energy Agency (2025) Global critical minerals outlook 2025. Paris: IEA.

Reuters (2025) West scrambles to fill heavy rare earth gap as China rivalry deepens. 19 November.

S&P Global (2026) Rare earth supply bottlenecks set to persist in 2026. 27 January.

US Geological Survey (2026) Mineral commodity summaries 2026. Reston, VA: USGS.

Wang, S. (2026) Optimizing Working Capital Management for SMEs.

Wetzel, P. and Hofmann, E. (2019) Supply Chain Finance and Corporate Performance.